A New York lawsuit is seeking to treat some of Bitcoin’s oldest dormant wallets, including addresses tied to the cryptocurrency’s creator, as lost property valued at less than $10 each.

The amended complaint asks a state court to grant legal ownership of 39,069 Bitcoin addresses to a pseudonymous plaintiff identified as Noah Doe and two Wyoming entities, ABC Company, and XYZ Company.

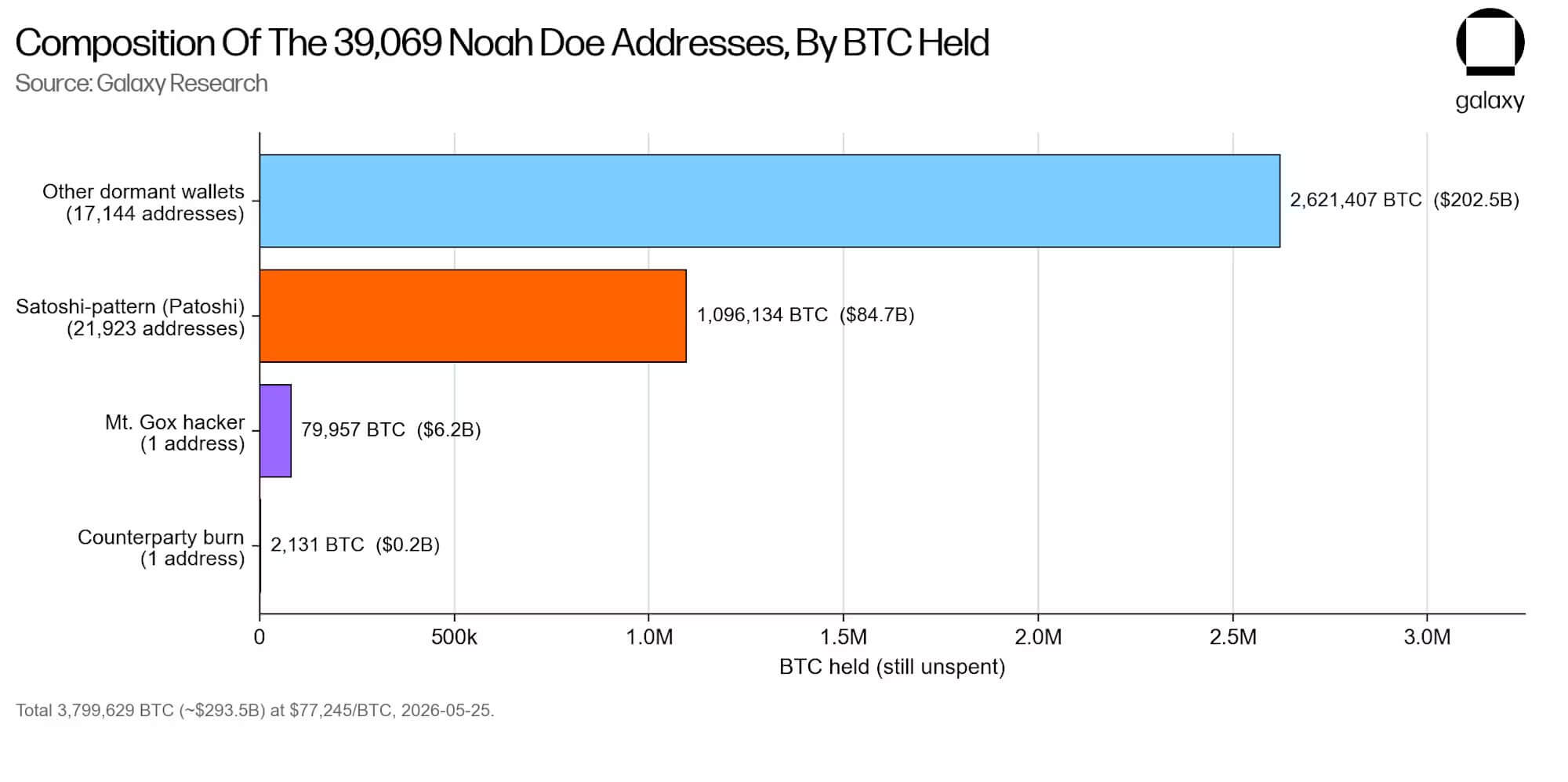

Together, the addresses hold nearly 3.8 million BTC, or about 18% of Bitcoin’s fixed 21 million token supply.

Galaxy Digital stated that nearly all of the 39,069 defendant addresses overlap with wallets that received small on-chain transactions in 2025.

At the time, Salomon Brothers used Bitcoin’s OP_RETURN feature to serve legal notices on the dormant wallets, claiming a right to seize them under the “Doctrine of Abandonment” unless the owners responded within 90 days.

After that campaign, hundreds of addresses moved coins and were excluded from the lawsuit. The addresses that stayed silent became the defendant set.

An old lost-property statute meets dormant Bitcoin

The plaintiffs’ case rests on an attempt to fit dormant Bitcoin addresses into New York’s lost-property law, a framework designed for physical items that can be found, reported, and returned.

Noah Doe and the two Wyoming-based entities argue that the wallets qualify as abandoned property because they were identified, reported to authorities, and left unclaimed for more than a year.

According to the complaint, the plaintiffs placed lists of the addresses on USB drives and delivered them to the New York Police Department’s 17th Precinct, then followed up with an on-chain notice campaign using OP_RETURN messages, a press release, and a claim window intended to demonstrate reasonable efforts to reach the owners.

The plaintiff’s legal effort leans heavily on Article 7-B of New York’s Personal Property Law, which allows a finder of lost property to claim title after the required holding period if no rightful owner appears.

In ordinary cases, that framework applies to property turned over to police and held while an owner is given time to come forward. The lawsuit asks the court to extend that logic to public blockchain addresses whose owners are unknown, unreachable, or silent.

To fast-track the litigation, the plaintiffs rely on a controversial valuation strategy, claiming an unnamed independent expert appraised the contents of each individual wallet at less than $10 because the private keys required to move the coins are unavailable.

Notably, New York law provides finders a shorter path to property worth less than $10 if they have made reasonable efforts to locate the owner and have failed.

However, on-chain data runs counter to that appraisal. Galaxy Digital stated that the 39,069 addresses hold an estimated $293.5 billion in Bitcoin at current market prices.

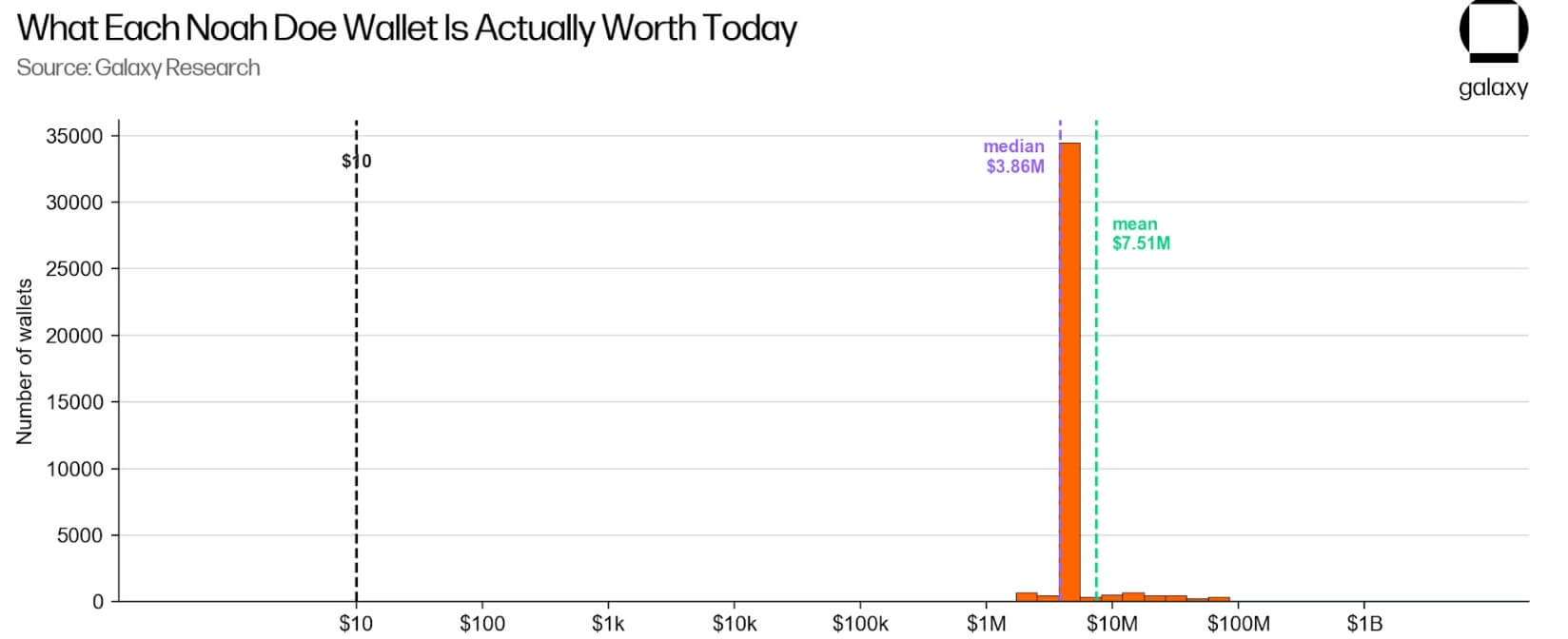

A further breakdown of the wallets showed that the average address in the legal claim contains 97.25 BTC, worth roughly $7.5 million, while the median holds exactly 50 BTC, or about $3.86 million.

That 50-BTC median reflects Bitcoin’s original mining reward, meaning many of the defendants appear to be early block payouts that have remained untouched since the network’s first years.

That gap between the legal valuation and current market value sits at the center of the dispute. If the court accepts the plaintiffs’ view that each address is worth less than $10 because recovery is uncertain, they can argue that the title vested one year after each batch of addresses was found.

However, if the court values the property by the Bitcoin recorded at those addresses, the lawsuit becomes far harder to place on the expedited track the plaintiffs are using.

The wallet list reaches Bitcoin’s earliest history

The addresses named in the lawsuit stretch back to Bitcoin’s earliest years, pulling some of the network’s most-watched and contested wallets into a claim built around abandonment.

Galaxy Digital said the defendant list is anchored by roughly 21,923 Patoshi-pattern addresses, a group of early-mined wallets long associated with Bitcoin’s pseudonymous creator, Satoshi Nakamoto.

Those addresses hold about 1.096 million Bitcoin, making them one of the largest dormant pools of BTC on the ledger.

Their inclusion gives the case its market significance, but it also complicates the plaintiffs’ theory.

Satoshi-linked coins are not obscure assets that disappeared from view. They have been studied for years by researchers, investors, and forensic analysts because any movement from those wallets would likely become one of the most closely scrutinized events in Bitcoin’s history.

Meanwhile, another target is a wallet holding 79,957 Bitcoin that blockchain investigators have linked to the 2011 Mt. Gox breach. Those coins are widely treated as stolen and contested property, a status that sits uneasily with a lost-property claim based on abandonment.

Additionally, the list also includes a counterparty-linked burn address holding 2,131 Bitcoin. Burn addresses are used to remove coins from circulation by sending them to destinations that cannot be spent from.

In that case, the legal claim runs into a technical wall because the address was designed so that no owner could later appear with a private key and move the funds.

Many of the remaining wallets last moved between 2009 and 2013, when Bitcoin went from having no market price to trading at a few hundred dollars. Some may belong to early miners. Some may reflect lost keys. Others may be cold storage, estate assets, or wallets controlled by holders who have chosen not to move their coins.

That uncertainty goes to the center of the dispute. Bitcoin’s ledger records movement, not intent. A wallet can sit untouched for 15 years because the owner is gone, because the key is lost, because the coins are deliberately held, or because the address can never be spent from at all.

The lawsuit asks a court to infer abandonment from inactivity, even though the blockchain alone cannot explain why a coin has remained still.

That mix shows the difficulty of applying a physical lost-property statute to blockchain records.

A judgment would create leverage, not control

Market analysts emphasize that even a sweeping courtroom victory for the anonymous plaintiffs would not immediately move a single satoshi.

This is because a judicial decree cannot generate the private cryptographic keys required to authorize a transaction, nor can it override the immutable math of a decentralized network.

Instead, the true value of a favorable judgment lies in its utility as a legal weapon at the boundary between Bitcoin’s permissionless ledger and traditional financial institutions.

If Noah Doe secures a quiet-title declaration from a New York court, that document would serve as a powerful cloud on title.

Should the legitimate owner of a targeted wallet ever move their Bitcoin to a centralized exchange, an institutional custodian, or a commercial bank, the plaintiffs could present the court order to freeze the accounts. This would trigger protracted domestic litigation, forcing the true owners to step forward and prove their identities.

That dynamic exposes a profound irony at the heart of the case. The plaintiff obtained permission from Justice Kathy J. King to proceed under a pseudonym, citing the threat of physical violence or kidnapping if his identity were tied to a multi-billion-dollar claim.

Yet, the legal mechanism he is employing forces the actual owners of the dormant wallets to forfeit their own privacy and expose their identities to the public record simply to defend their property.

Because the defendants are anonymous cryptographic addresses, no traditional defense counsel is expected to appear in court.

Galaxy Digital stated that a technical default is likely by late June 2026, roughly 30 days after the on-chain service of process was executed, with a formal motion for a default judgment anticipated later this summer.

However, the firm argued that a rubber-stamped victory is highly improbable. New York justices retain broad discretion when evaluating applications for declaratory judgments, particularly when confronting novel legal frameworks, questions regarding process servers, and a nominal $10 valuation slapped onto a $293 billion fortune.

Alex Thorn, head of research at Galaxy Digital, concluded:

“It would be extraordinary for a New York court to hand three anonymous parties legal title to roughly $293 billion worth of BTC, including the coins most closely associated with Satoshi Nakamoto, on a lost-and-found theory propped up by a questionable under-$10 valuation,”

Credit: Source link